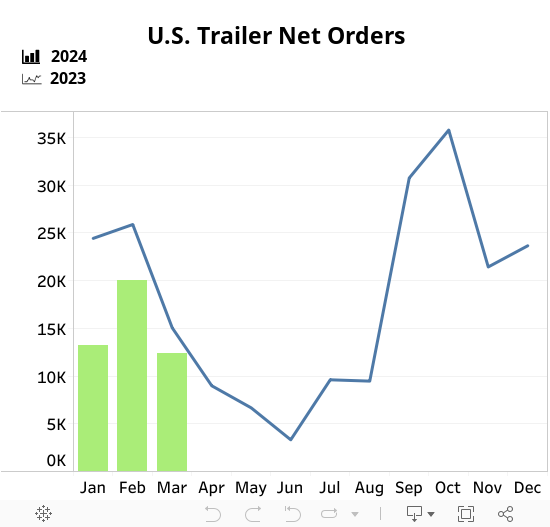

FTR Reports Trailer Net Orders Edge Higher in May to 20,189 units

U.S. trailer demand was resilient in May, increasing 1% month over month (m/m) to 20,189 units, which represented a surge of 249% year over year (y/y) versus a very weak level in May 2025, FTR reported. Orders were far above the 10-year May average of 11,649 units, indicating better-than-seasonal momentum into late spring. Dry van trailers led the strength, but other key trailer types were strong as well, and almost all logged improved orders from a year earlier.

U.S. trailer builds declined 6% m/m in May to 16,553 units and were down 1% y/y, showing that trailer manufacturers remain cautious despite improved orders. Production for the year to date was essentially flat y/y at 79,482 units as net orders continued to outpace build.