FTR Reports U.S. Trailer Orders in June Reflect Solid Demand at 14,474 Units

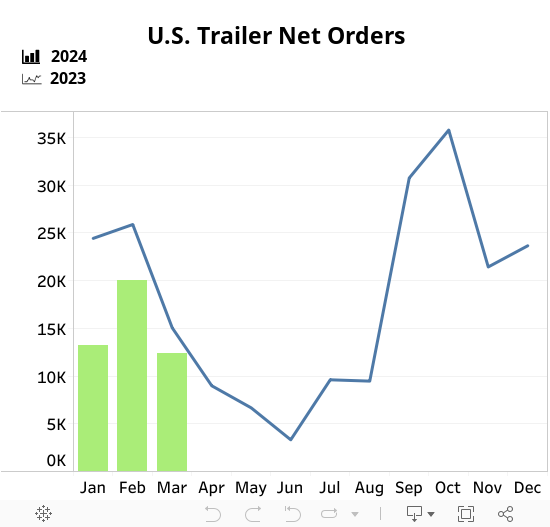

U.S. heavy-duty trailer demand cooled in June but remained solid for a seasonally slow month. Net orders fell 28% month over month (m/m) to 14,474 units but rose 14% year over year (y/y) and were 8% above the 10-year June average of 13,379 units. The pullback likely indicates that April and May’s stronger intake was temporary rather than a new run rate. With summer typically weak, demand is unlikely to improve meaningfully until 2027 order boards begin opening around September. Refrigerated van and flatbed orders drove most of June’s y/y growth while dry van demand weakened after several solid months of orders. Almost all other segments improved from last year.

June builds rose 6% m/m to 17,633 units but were 1% below last year. Year-to-date production was nearly flat, down 0.5% y/y to 97,165 units. Overall, manufacturers remain cautious and are keeping production aligned with demand.

The market remains in a selective, replacement-driven recovery rather than a broad capacity expansion cycle. Stronger freight rates are supporting fleet confidence, but freight volume growth remains limited, and many carriers are still rebuilding margins. Low cancellations point to stable order commitments while strong Class 8 demand is diverting some fleet capital from trailers. Excess trailer capacity, high financing costs, elevated equipment prices, and uneven profitability will likely keep the recovery gradual.