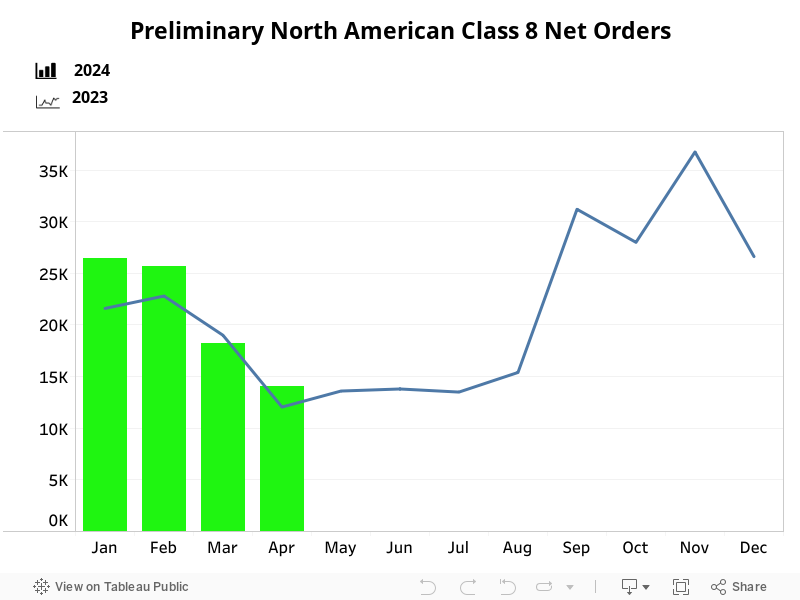

Preliminary North American Class 8 Net Orders for July Were Down 31% from June at 22,000 Units

FTR reports that North American (N.A.) Class 8 preliminary net orders subsided in July to 22,000 units, down 31% from June but up 75% year over year (y/y). Replacement demand, firmer freight rates, improving utilization, and a moderate pre-buy to avoid new emissions changes continue to support the market. However, most calendar 2026 truck production is already committed, and manufacturers have yet to open 2027 order boards, so build slots are constrained.

Through July, net orders for 2026 to date were up 120% compared to the same period last year. Orders for the current order season, measured from September 2025 through July 2026, were up 39% y/y. Class 8 orders totaled 344,823 units over the past 12 months.